Trend and Application of Green Technology Innovations Development in China

This document is for:

-

European SMEs and start-ups who provide innovative methods or ideas to tackle the challenges for the green technology adoption in China

-

European SMEs and start-ups that are focused on the green technology sector or related technologically features e.g. renewable energy, green building, etc.

Overview

Green technology has gained prominence over the last two decades. Green technology, also known as “environmental technology” or “clean technology”, refers to all the environmentally friendly technologies which do not disturb the environment or destroy natural resources. As our planet starts to suffocate from all the pollution we create and its natural resources are drying up, the active use of green technology can help significantly reduce ecological impacts and resource intensity, thereby contributing to balancing environmental protection and economic development, which is the key to the creation of a sustainable society. This is the reason why the developed and some of the developing countries are now turning to this type of technology and it has become one of the fastest growing sectors of employment.

The importance of green technology has increased worldwide, especially in China. China has experienced rapid economic development after years of heavy industrialization. The factories and power plants that have driven its economic growth are energy and natural resource intensive and produce a significant amount of environmental hazards. Consequently, China has been the world’s largest greenhouse gas (GHG) emitter since 2006 and domestically the quality of the water, soil and air is severely compromised – about 80% of groundwater in the nation’s major river basins is unsafe for human contact; 16.1% of China’s surveyed land is polluted by heavy metals; Chinese cities, particularly the ones in northern China, are often surrounded by toxic smog caused by industrial discharges, coal burning and car emissions, among others. Faced with huge and growing energy needs and environmental and energy security challenge, China is currently in need of developing green technologies which will help the country to produce cleaner energy and to consume it more efficiently.

China appears to be genuinely committed to addressing climate change, resolving pollution problem and promoting green-tech innovation. Green growth is prioritized in China’s 13th Five-Year Plan (FYP) (2016-2020) which sets goals and plans to encourage clean energy production and consumption. In this plan, the Chinese government has further tightened targets for energy intensity, renewable energy share, and carbon intensity compared with the 12th FYP. In addition, the country’s “Belt and Road Initiative” sets “ecological civilization” as a primary goal, which means it will foster the flow of clean technologies between borders and promote global collaborations for a low-carbon economy. These measures, together with all the other policies and campaigns the nation has launched to strengthen and extend its efforts for green development, are expected to unlock substantial opportunities for domestic and European players in the green tech sector, especially for those in the fields of water, air and soil monitor and control, renewable energy, new energy vehicles, and waste management.

Important!

Most important things to know about green technology innovation in China

-

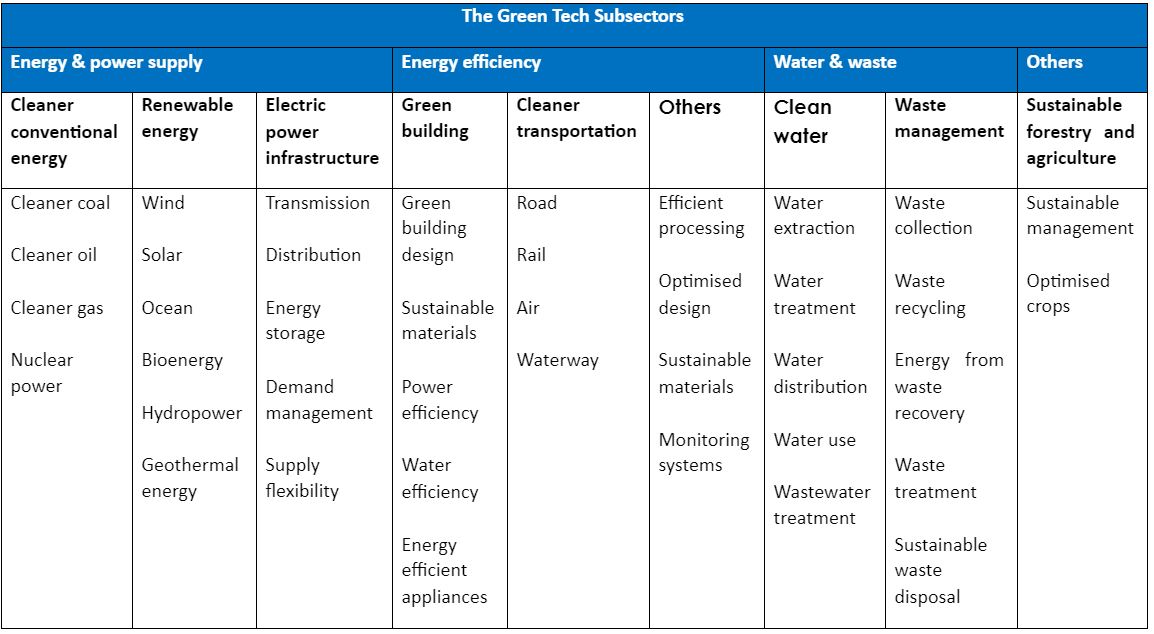

The green tech subsectors – green technology covers a wide range of production and consumption technologies. The table below provides a brief overview of the green tech subsectors in China.

Source: EU SME Centre & NRDC

-

Challenges

-

Lack of mature technology: developments such as the exploration of large scale solar generation and offshore wind in deep-water locations entail significant risk and uncertainty.

-

Lack of mature market: the market for renewables is volatile and companies must manage frequent demand-supply imbalances caused by cyclical factors such as oil prices and one-time events (e.g. the Japanese nuclear crisis).

-

A variable of government subsidies: companies need to cope with a variable of government subsidies because a significant component of the green industry’s growth, particularly in solar sector, is driven by government incentives.

-

On Level 2 you can find information about trend and application of green technology innovations development in China, while Level 3 will tell you more about business activities (through case studies) in green technology innovation development in China and what the EU has contributed in China.

This page will offer a brief overview of the current green technology industry and its development in China. The main focus will be given on green technology research development, the existing sustainable development zones, and renewable energy development in this country.

China is fully embracing green technology and emerged as the largest producer and consumer of green tech in the world. The central government has consistently shown its willingness to invest heavily in green industries to tackle pollution and introduce investment incentives and preferential policies to foster domestic clean-tech market as well as attracting overseas investors. A significant amount of money has been poured into the green tech sector – China’s investment in clean technology and renewable energy has exceeded the combined total for Europe and the United States and is estimated to reach 17 trillion RMB (approx. EUR 2 trillion) by 2020, with an increase of RMB 2 trillion (approx. EUR 245 billion) each year. Thus this sector is of huge market potential.

Green technology research and development in China

Green technology innovation in China is becoming more mature compared to the initial stage ten years ago. Most contributors to the development are Science and Technology universities or organisations, especially the universities from “985” and “211” project. However, the qualitative publications dominate the researches while the empirical researches are in shortage, which indicates the green technology innovation in China is still at a developing stage and needs more executions. The research subjects are multi-perspective and multi-disciplinary, the majority of which fall on environment science, management, energy and fuels, economics and social behaviour. The trend of green technology research is toward interdisciplinary research in the fields related to the environment, science technology, business economics, engineering, and energy and fuels.

Sustainable development zones

Three sustainable development zones were approved by the Chinese government in 2018, which will implement the United Nations 2030 Sustainable Development Goals: the first one is in Shenzhen, China’s innovation engine. This zone will integrate technologies in sewage treatment, waste utilization, ecological restoration, and artificial intelligence, with the aim of solving issues from resource management to pollution; located in Guilin and targeting desertification, the second zone will foster innovative solutions that can be replicated by other regions faced with the threat of encroaching deserts; the third one is in Taiyuan, which will focus on innovations that tackle air and water pollution, producing solutions that can be replicated by regions relying on resource extraction.

Renewable energy development in China

China sees renewable energy as the way of the future. For more than half a century, the country has relied heavily on fossil fuel, particularly on coal, to offer energy to its citizens and to power its industry. However, fossil fuels are non-renewable resources and the effects of such a massive use of them on the environment have proved devastating. Since 2013, severe air pollution and climate change fears have made the country turn to alternative renewable energy sources that are more environmentally friendly. China has set two important targets in renewable energy development – to increase the share of non-fossil fuels in primary energy consumption to 15 percent by 2020, and to about 20 percent by 2030; to increase the share of installed non-fossil fuel generation capacity to about 39 percent by 2020. In addition, China’s National Energy Administration (NEA) and the National Development and Reform Commission (NDRC) plan to invest more than US$ 360 billion (approx. EUR 307 billion) in developing renewable energy, which will generate 13 million additional jobs in this sector by 2020.

China is already in a leading position in renewable energy output. Hydro remains the leading renewable power source in the country, but the greatest growth has been observed in solar and wind energy. China is currently the world’s biggest producer of wind and solar power energy and under its 13th FYP, it aimed to have 110 gigawatts (GW) of solar capacity and 250 GW of wind power capacity installed by 2020. By 2017, China has already reached the target of installing 110 GW of solar, thus the target has been increased to 200 GW by the Chinese National Renewable Centre. On the wind front, the estimated generation capacity by 2020 is now set at 264 GW, which surpasses the original target set in the 13th FYP. Foreign investment in solar and wind technology has been encouraged by the government to support the country in meeting its ambitious capacity targets. A variety of incentives are in place, which include reduced corporate income tax rates for installing wind power in the country’s western regions.

Recently, more focuses have been put on the consumption of renewable energy as much of the clean energy China produces was lost to curtailment, due in large part to outdated power grid. Back in 2016, wind curtailment reached a high of 17 percent for the full year and in some provinces such as Gansu, 40 percent of wind energy was lost to curtailment. A policy introduced in 2016, Document 625, included requirements for compensation for curtailment of renewable energy, which was re-emphasized in late 2019. In 2018 the government also identified a target for provinces and grid firms to steadily reduce wind and solar curtailment, with a goal of curtailment below 5 percent in all provinces for both wind and solar. Therefore, business opportunities may exist for European companies with expertise in the development of smart grids – electric grids that use big data and advanced technology to deliver electricity in a more reliable and efficient way.

This section will centre on relevant EU and Chinese stakeholders and their actions contributing to the development of renewable energy. The contributions from the EU will be highlighted in particular, most of which have been made through S&T collaboration with China.

Presence of local and global companies contributing to renewable energy development

Local state-owned enterprises (SOEs) and private companies have been contributing to the development of renewable energy in China. The well-known China Three Gorges Corporation (CTG), a Chinese SOE established in 1993, has taken full responsibility for the construction and operation of the Three Gorges Project and four large-scale hydropower stations located in the upper reaches of the Yangtze River. Apart from hydropower operation and development, it is also specialising in the development of new energy like wind and solar in both China and abroad. In terms of private companies, Trina Solar, a Chinese company and the largest solar panel manufacturer in the world, has broken the world record on the efficiency of multicrystalline-silicon solar cells, and delivered more than 50 GW of solar modules worldwide as of June 2020. Given that Chinese local manufacturers are well developed and positioned on the market, European companies ought to enter the market with advantages in technology, efficiency, and expertise, which will make them attractive for joint ventures with Chinese partners or allow them to sell directly to private entities.

In addition, some global corporations like Canadian Solar, GE Wind Energy and Vestas Wind Systems have also been major players in the renewable energy sector in China. Vestas Wind Systems, headquartered in Denmark, has secured a 50 MW order from CTG Renewables, which includes supply of 15 V155-3.3 MW turbines with 142 m towers, as well as a 5 -year Active Output Management 5000 (AOM 5000) service agreement. With this order, the Danish company has secured over 300 MW of order intake of the V155-3.3 MW turbine in China.

EU- China Collaboration in Renewable Energy Innovation

An annual energy dialogue has been set up since 1994 for EU and Chinese officials to cooperate on energy-related issues. The dialogue's work often forms part of the annual EU-China summit, with the last energy dialogue held between Commissioner Miguel Arias Cañete and Administrator Zhang Jianhua in 2019. Four priority areas for cooperation have been identified with the aim to further advance the clean energy transition:

-

energy efficiency

-

renewable energy sources

-

design and transformation of the energy system

-

the role of innovative actors

The energy dialogue was deepened and intensified by the 2019 Joint Statement on the implementation of the EU-China cooperation, which follows the EU-China roadmap on energy cooperation (2016-2020), signed in 2016, and the leader’s joint statement on climate change and clean energy, endorsed in 2018. Examples of EU-China Cooperation in renewable energy development are provided below.

ECECP was launched in Beijing on 15 May 2019, after its implementation was endorsed by the EU and Chinese leaders, Presidents Juncker and Tusk and Premier Li in the EU-China summit statement, 9 April 2019. The platform will gather a wide range of energy players in China and the EU, resulting in a thorough analysis of the benefits and challenges in all the four priority areas, as identified in the joint statement from 2019. It will also create opportunities for political and policy exchange as well as new business prospects for innovative companies in energy sector.

-

There are several EU-China H2020 projects working on the development of renewable energy sources and reduction of GHG emission which include: InnoDC, eCOCO2, COZMOS, ComBioTES, HySEA, BIOMASS-CCU, SUN2CHEM and NoAW. Below are further descriptions of selected projects:

-

InnoDC (H2020 project)

-

At present, renewable energy sources are increasing their share of electricity generation. This is particularly the case for offshore wind energy. The project focusses on the development of the electricity transmission system, targeting the connection of offshore wind, the integration of offshore wind with the existing power system (including the use of HVDC), and the operation of the future power system where large scale wind is connected to a hybrid AC and DC power system. Cardiff University is the project coordinator and the consortium comprises a total of 15 institutions, of which 14 are European and one partner from China.

-

-

BIOMASS-CCU (H2020 project)

-

The BIOMASS-CCU consortium aims to maximize the environmental benefit of carbon emission, and enhance the economic feasibility by producing high value alkenes from CO2 using conventional and advanced non-thermal catalysis. Additionally, through the combination with energy storage and novel heat exchange approaches, energy efficiency of biomass gasification will be significantly enhanced. Extensive techno-economic and life cycle analysis will be carried out to justify the advantages of the proposed biomass gasification technology. The project is led by Queen’s University of Belfast, and the consortium comprises a total of 15 institutions, of which 8 are European, 5 are from China and two partners from Australia.

-

-

COZMOS (H2020 project)

-

Greenhouse gas CO2 could be captured from industrial waste streams and turned into a valuable raw material. Its transformation is currently hindered by the low CO2-to-product yield. The EU-funded COZMOS project will overcome this by combining two reactions into one reactor to increase the CO2 conversion rate and reduce energy consumption. The transformation of CO2 sourced from renewable energy sources will lead to the production of propane – a fuel that can be easily stored for use in heating, cooking and transportation – or propene, which forms the basis of lightweight plastics. COZMOS technology will contribute to a circular economy and the replacement of fossil fuels, leading to a decrease in CO2 emissions and reduced European dependence on fossil fuel-based resources. The project is led by University of Oslo, and the consortium comprises a total of 12 institutions, of which 10 are European, one from China and one from Saudi Arabia.

Sources

https://usgreentechnology.com/need-green-technology/

https://www.theenvironmentalblog.org/2018/04/green-tech-future-mankind/

https://www.g20-insights.org/policy_briefs/innovative-green-technology-s...

https://www.intechopen.com/books/innovation-in-global-green-technologies...

https://www.sciencedirect.com/science/article/pii/S0048969719339853

http://www.iberchina.org/files/china_green_tech.pdf

https://www.eusmecentre.org.cn/article/china’s-green-tech-market-business-opportunities-and-market-access-advice-eu-smes

https://www.nrdc.org/stories/renewable-energy-clean-facts

http://usa.chinadaily.com.cn/business/2013-02/08/content_16215049.htm

https://ui.adsabs.harvard.edu/abs/2020E%26ES..467a2207L/abstract

https://www.weforum.org/agenda/2018/04/china-is-going-green-here-s-how/

https://www.asiapacific.ca/blog/chinas-clean-tech-commitment

https://www.csis.org/east-green-chinas-global-leadership-renewable-energy

https://www.pwccn.com/en/industries/energy-utilities-and-mining/renewable-and-cleantech.html

https://www.pwccn.com/en/energy-utilities-mining/chinese-cleantech-market-opportunities-2017.pdf

https://www.researchandmarkets.com/r/7b8wzs

https://www.oecd.org/env/country-reviews/PR-China-Green-Growth-Progress-Report-2018.pdf

https://www.carbonbrief.org/china-leading-worlds-clean-energy-investment-says-report

https://www.hydropower.org/companies/china-three-gorges-corporation

https://news.cision.com/vestas-wind-systems-a-s/r/vestas-wins-order-for-...

https://ec.europa.eu/energy/sites/ener/files/documents/FINAL_EU_CHINA_ENERGY_ROADMAP_EN.pdf

https://ec.europa.eu/energy/topics/international-cooperation/key-partner...